Block’s Layoffs Reveal the Dark Side of the AI Economy

One fintech company cut 40% of its workforce. The rest of the knowledge economy may soon follow.

Thousands lost their jobs last week. And investors celebrated.

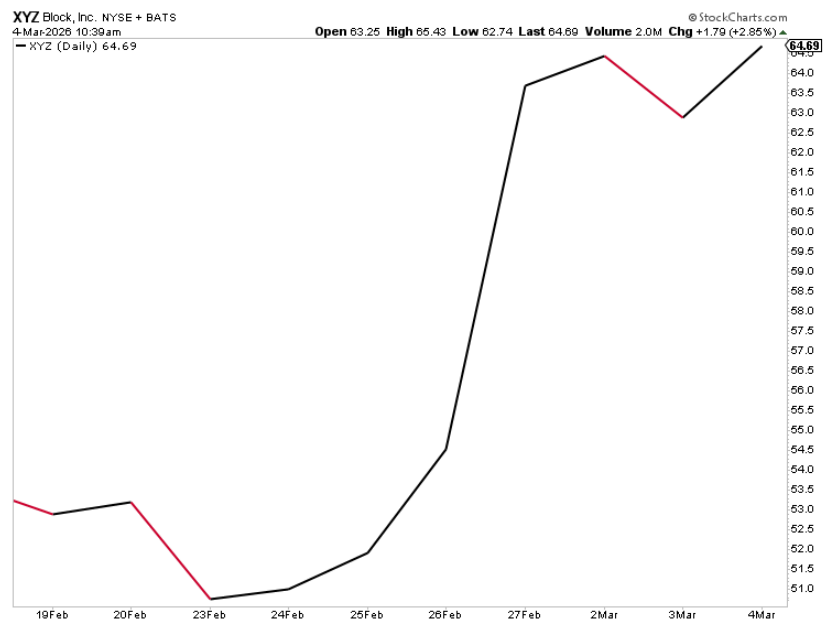

When Block (XYZ) announced it would eliminate 4,000 employees – roughly 40% of its workforce – the stock surged 24% after hours and added billions of dollars in market value.

In almost any other era, that reaction would have seemed grotesque. Today, it looks like a preview of the AI economy.

This shockwave didn’t come because the business was struggling but because, in Dorsey’s own words, “intelligence tools have changed what it means to build and run a company.”

And it tells us almost everything we need to know about what is coming…

Because this wasn’t just a layoff announcement.

This was a signal.

While companies cut staff all the time – restructurings, downturns, pivots, the occasional spectacular implosion – this was different in kind. Dorsey didn’t apologize his way through a financial crisis. He didn’t blame macroeconomic headwinds or “right-sizing” for a post-pandemic reality. He said, plainly and with apparent genuine conviction, that AI had made thousands of his employees unnecessary – and that within a year, most CEOs would arrive at the same conclusion.

“I’d rather get there honestly and on our own terms,” he wrote, “than be forced into it reactively.”

He’s probably right. And that is exactly the problem.

The Competitive Domino Effect Now Facing Fintech

Let’s be clear about what likely happens next.

Block’s direct competitors – PayPal (PYPL), Shopify (SHOP), Stripe, Adyen (ADYEY), Clover, Toast (TOST) – are watching this announcement very carefully. Dorsey just gave them cover.

The moment one major player in a competitive market achieves structurally lower operating costs through AI-driven headcount reduction, the others face a binary choice: match the efficiency or compete at a permanent cost disadvantage. In a low-margin, high-volume industry like payments, that’s not really a choice at all.

So, fintech will cut. Then the competitive pressure radiates outward to the broader financial services sector – to the payment processors, banks, insurance companies, and asset managers who have been nervously watching AI productivity metrics for two years and quietly hoping someone else would go first.

Block just went first. Others will follow.

The logic that applies to fintech also applies to software, consulting, media, law, accounting… any industry where people are paid to think.

That is the knowledge economy. It employs tens of millions of Americans across finance, technology, consulting, media, and professional services.

And it is now facing an existential crisis from AI.

You see – Dorsey didn’t just fire 4,000 people. He fired the starting gun.

To understand how large that shift could become, we ran the numbers.

Modeling the AI Layoff Scenarios

Using Block as an anchor, we modeled the employment implications across three frameworks. The results are not encouraging.

Framework 1: Pre-COVID Headcount Reversion

At the end of 2019, Block employed 3,835 people. It grew to over 10,000 by 2025 – a 174% increase – before cutting back to 6,000. If AI allows companies across the knowledge economy to revert to their pre-pandemic headcounts, the math implies a moderate but significant employment shock.

Depending on how aggressively you model the overhiring and how many displaced workers find new roles, total U.S. unemployment could plausibly land somewhere between roughly 5% and 8% – a mild-to-severe recession range.

This is the most conservative framework, because most knowledge economy companies didn’t grow as aggressively as Block during COVID.

Framework 2: Revenue-Per-Employee Shock

Block’s post-cut revenue per employee improves by roughly 75% relative to its pre-cut level. Apply that productivity gain – scaled to realistic adoption rates across the broader knowledge economy – and you get potential unemployment outcomes between 8% and 16%, with the middle scenario of 50% productivity gains producing roughly 12% total unemployment.

That exceeds the peak of the 2008 financial crisis.

Framework 3: The 40% Headcount Reduction Scenario

If we assume fintech follows Block, cutting 40% of headcount, and the broader knowledge economy achieves a 30- to 40% reduction, total unemployment could run 9% to 13%, with the moderate-to-aggressive scenarios consistently pushing above 10%.

Across all three frameworks, the most likely range is 8% to 13% total U.S. unemployment – with the most defensible central case somewhere around 10- to 11%.

To be precise: these are total unemployment rates, including today’s baseline of 4.2%. The AI-attributable increment is roughly six to nine percentage points above the current level.

In these scenarios, the unemployment rate for the knowledge economy in particular runs between 15- and 23%. Think about that. College-educated, white-collar professionals – the people who were told that education was the hedge against technological displacement – experiencing Great Depression-era joblessness in their specific labor market.

These are the hard numbers we could soon be facing if Block just created the new labor framework for the Age of AI.

Why AI Job Losses Could Be Structural – Not Cyclical

In every recession throughout American history, the implicit promise has been that the jobs come back.

Cyclical unemployment is painful but temporary. The economy contracts, the Fed cuts rates, demand recovers, hiring resumes. In most downturns, displaced workers eventually find their way back into the labor market. After the COVID shock of 2020, for example, restaurant employment rebounded quickly once demand returned. Even after deeper recessions, new jobs eventually emerge to absorb displaced workers.

But what Block has announced is not cyclical. It is structural. The jobs are not coming back because the need for those jobs no longer exists. A 50-person team doesn’t need to regrow from 30 when the economy recovers – it can stay lower because AI handles what the other folks used to do. The productivity gain – and the displacement – is permanent.

This means the traditional escape valves don’t work.

Retraining into the skilled trades is often floated as the obvious solution. And for some displaced workers, it will be. But large-scale labor transitions rarely happen as smoothly as policy discussions suggest. Skilled trades require years of apprenticeship, physical conditioning, and geographic flexibility – not something millions of mid-career professionals can pivot into overnight. And even that path may not be immune for long.

The next wave of AI isn’t just software; it’s robotics. Companies from Tesla (TSLA) to Figure AI are racing to scale humanoid robots designed specifically for physical work. If those systems mature over the next decade, the same forces disrupting white-collar jobs today could eventually start reshaping parts of the trades as well.

And the “AI creates new jobs” argument, while historically valid in other technological revolutions, faces a structural challenge it has never faced before. Every previous automation wave left humans with a comparative advantage in creativity, judgment, and complex reasoning. AI is attacking precisely those capabilities. The historical analogy may simply not hold.

What we would get instead is bifurcation. A small cohort – perhaps 10- to 15% of displaced workers – successfully pivots to AI-adjacent roles: prompt engineering, AI training, model evaluation, the genuinely irreplaceable functions of high-trust human relationship management.

The rest face a very different reality – one the American social contract has little institutional language for.

What a 10% AI-Driven Unemployment Economy Might Look Like

Believe it or not, in this scenario of ~10% structural unemployment, GDP probably looks fine. Maybe even good.

Productivity gains flow into corporate output, margins expand, earnings grow, and GDP – which measures production, not welfare – ticks upward at 2- to 2.5% annually. The headline number will be used, relentlessly, to argue that everything is working. It is not a lie. It is something worse than a lie: a true statement that obscures a catastrophe.

The stock market, in the near to medium term, goes up. Every Block-style announcement is a double-digit after-hours pop. Every CEO who announces AI-driven headcount reductions is rewarded by shareholders. The S&P 500 could be at 7,000… 8,000… even 9,000… while 12% of the country is structurally unemployed.

Both things will be true simultaneously. The cognitive dissonance will be extraordinary.

Wealth inequality moves from “already alarming” to “historically unprecedented.” The labor share of GDP – currently around 60% – compresses toward 45- to 50% as productivity gains accrue to capital rather than workers. Stock ownership, concentrated overwhelmingly in the top 10% of the wealth distribution, means that rising markets directly transfer wealth upward.

The U.S.’ Gini coefficient – a measure of income inequality where 0 represents perfect equality and 1 represents maximum inequality – is already among the highest in the developed world at 0.49. Wealth inequality is even more pronounced, with a Gini coefficient of roughly 0.83. Both could continue rising toward levels historically associated with periods of significant social and political instability.

That is the future. And it seems imminent.

The Petro-State Parallel: When Capital Replaces Labor

Step back from the modeling for a moment, and the bigger structural shift comes into focus.

There is a historical analogy for an economy that generates enormous wealth from a highly productive, capital-intensive sector that employs relatively few people: the petro-state.

Saudi Arabia. Kuwait. Venezuela before its collapse. In these economies, oil – not labor – created most of the national wealth.

The oil sector itself employed surprisingly few people compared to the wealth it generated. Governments often redistributed that wealth through public-sector jobs, subsidies, and social programs.

The emerging AI economy could start to resemble parts of that structure.

A small number of companies – the hyperscalers, the foundational model providers, the AI-native platformers – generate extraordinary output with minimal labor. The core infrastructure layer of the AI economy simply may not require millions of workers.

That raises a question resource economies have faced for decades: if a narrow slice of the economy generates most of the wealth, what role does everyone else play in the system?

Many petro-states addressed that imbalance through redistribution funded by resource revenues, often alongside highly centralized – sometimes authoritarian – political systems. In many Gulf states, resource wealth effectively purchased social stability. Citizens received economic benefits funded by oil revenues while political participation remained relatively limited.

The United States could face a version of this tension from a very different starting point.

The workers most exposed to AI disruption are not populations that historically expected redistribution. They are knowledge workers who were told – repeatedly – that education was the path to economic security. Many accumulated significant student debt on that premise. They built professional identities, social status, and financial lives around the assumption that the knowledge economy would continue to need them.

If that assumption changes quickly, the adjustment could be complicated.

Modern advanced economies have very little precedent for navigating this kind of transition. And policymakers are only beginning to grapple with what it might mean.

Who Wins In the AI Economy

Feb. 26, 2026 may eventually be remembered as an early signal that the structure of human labor was beginning to change, and Block’s Dorsey was simply the first to act on it honestly.

The restructuring of the U.S. labor market that follows will produce an equally fundamental restructuring of the U.S. economy. The specific contours remain genuinely uncertain. The political response – ranging from aggressive redistribution to authoritarian reaction to some combination of both – will shape the outcome as much as the technology itself.

The timeline, magnitude, and societal repercussions remain unclear.

What is decisively not unclear is who benefits from the transition itself, regardless of how it resolves.

The companies that build the infrastructure of the AI economy – the foundational model makers, the hyperscalers who provide the compute, the semiconductor manufacturers whose chips are essential to this new economy, the energy companies and data center builders who power the whole apparatus – are the functional equivalents of whoever held the mineral rights when oil was discovered.

In a world where intelligence becomes a commodity produced by machines, the machines – and the companies that own them – win.

The question of what happens to everyone else is the most important political and social question of our lifetimes.

It doesn’t have an answer yet. But Jack Dorsey just forced it into the open.

And while policymakers argue about the consequences, the investment implications are already becoming clear.

The companies building the infrastructure of artificial intelligence – the models, the chips, the data centers – are becoming the economic backbone of the next era.

And the company most closely associated with that transformation may soon give investors their first real chance to buy in.

OpenAI is widely expected to enter public markets this year. When it does, it could become the first true “AI platform” stock – the equivalent of owning the operating system of the intelligence economy.

I’ve identified a way investors may be able to position themselves before that moment arrives – before the IPO headlines, before the Wall Street frenzy, and before passive funds rush in.

You can learn how it works right here.